UK cryptoasset regulation is taking shape: Key developments and what firms must do now

16 Apr 2026 • Financial Services • ICARA and wind-down processes • Insight • Preparation of Disclosures • Prudential Reporting and Advisory • Regulatory Reporting • Thresholds, indicators and OFAR monitoring • Transparency Reporting

Written by

The journey towards a fully regulated UK cryptoasset framework continues at pace. The Financial Conduct Authority (FCA) has provided more information on the authorisation process and how the application gateway will operate when it opens on 30 September 2026, with the regime becoming fully operational from 25 October 2027.

Following our earlier insight on the FCA’s vision for crypto regulation, a series of key publications have refocused the industry’s attention on the rules, expectations and operational commitments that authorised firms will soon face. These include Consultation Paper CP26/4, Quarterly Consultation CP26/8, and the FCA’s updates on the application period. Collectively, these developments outline a far more rigorous environment, one that requires forward‑planning, technical understanding and investment in a robust governance framework.

Below, we summarise the recent consultations and set out what firms should be thinking about and doing to ensure they are prepared once the application window opens later this year.

CP26/4 – Application of the FCA Handbook for Regulated Cryptoasset Activities II

(Published 23 January 2026)

The consultation paper sets out how key components of the FCA Handbook will apply to firms undertaking regulated cryptoasset activities (cryptoasset firms):

Consumer Duty (the Duty)

The FCA is consulting on how the Duty should apply to firms, recognising that crypto markets operate differently from traditional finance firms. At the same time, the FCA is progressing with wider amendments to the Duty to reduce disproportionate burdens on wholesale firms, with this consultation running through the first half of 2026. As these changes are likely to evolve before the crypto regime goes live, firms are being encouraged to engage with these consultations now to help shape the final rules and ensure they can integrate the Duty effectively once authorised.

Conduct of Business Standards (COBS)

COBS will apply to firms to ensure consistently high conduct standards across the sector. The FCA sees this as essential to addressing existing risks such as unclear disclosures, misleading promotions, inconsistent client treatment and cyber-related vulnerabilities. By aligning crypto firms with the expectations placed on traditional investment firms, COBS will require clearer communications, stronger governance over customer interactions, and more robust controls around product information, fees and operational risks.

Senior Managers and Certification Regime (SMCR)

The FCA proposes applying the ‘Core’ and ‘Enhanced’ SMCR framework to cryptoasset firms, with thresholds designed to mirror those already used for high impact traditional finance firms. Under the consultation, a firm would fall into the ‘Enhanced’ category where it exceeds the following criteria:

Stablecoin issuance firms: A backing asset pool exceeding £65bn, calculated as a three-year rolling average. At present, the threshold captures assets under management of £50bn or more calculated as a 3-year rolling average and will be updated to £65bn subject to final responses to the separate SMCR consultation.

Cryptoasset custodians: Holding more than £100bn in combined client assets and safe custody assets in any given month over the previous year or projecting to exceed £100bn in any month of the current year. This mirrors the existing SMCR criteria for traditional custodians safeguarding £100bn or more of qualifying assets.

Prudential and regulatory reporting

The FCA are proposing that the existing returns in SUP 16 will apply to all qualifying firms that have Part 4A permission. New crypto‑specific returns will be introduced over the first few years of the regime and refined as necessary following engagement with firms. Firms will also be required to submit prudential returns, which will provide the FCA with visibility of capital and liquidity positions.

CP26/8 – Quarterly Consultation (Chapter 2 – Amendments to CASS related to cryptoasset activities)

(Published 6 March 2026)

CP26/8 the FCA sets out how the Client Assets Sourcebook (CASS) will interact with the new UK cryptoasset regulatory regime, aiming to avoid duplicative or conflicting obligations while ensuring robust consumer protection.

Key FCA proposals

Money held to back qualifying stablecoins would be brought within the CASS 16 safeguarding regime rather than CASS 7, requiring firms to hold such funds in accounts that are fully segregated from client money.

Removing the professional‑client opt‑out in CASS 7 for client money held in relation to qualifying cryptoasset activities.

Disapplication of the CASS 7 DvP exemption for cryptoasset transactions, since current crypto trading venue settlement arrangements do not qualify as commercial settlement systems.

The FCA also proposes specifying that references to designated investments in CASS 7.16.22E should be interpreted as including qualifying cryptoassets.

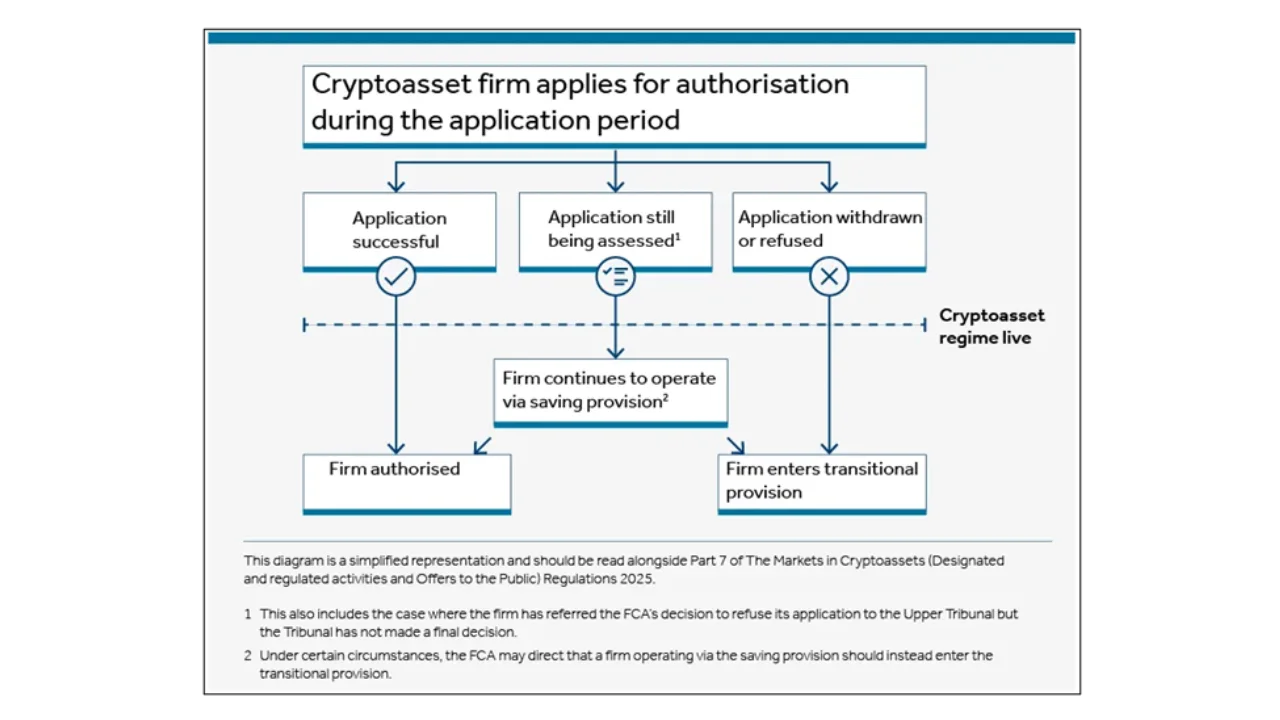

Getting authorised: How the application period will work

The application window for firms wishing to undertake cryptoasset regulated activities will run from 30 September 2026 to 28 February 2027.

The FCA states that where a firm applies during the application period, they expect to decide on the application before the new regime goes live. However, if this is not the case, a saving provision will apply that will allow the firm to continue to provide cryptoasset services until its application has been finally determined. Where an application is refused or withdrawn the firm will enter into a ‘transitional provision’ which will allow firms to run off their UK cryptoasset business and exit the UK market in an orderly manner.

The FCA’s illustration below sets out the possible outcomes for firms applying during the gateway period.

Note:

Application period 30 September 2026 to 28 February 2027

Cryptoasset regime to go live 25 October 2027

What cryptoasset firms should be doing now

With the gateway opening later this year, firms should now be moving from high-level planning to detailed preparation. Early engagement and clear internal coordination will be critical to ensuring a smooth application process and avoiding operational restrictions during the transitional period.

The FCA advises firms to focus on the following key actions:

Engage early with the FCA: A pre-application meeting offers firms valuable informal feedback on business models, activities and readiness. It also helps the FCA understand key risks in advance, reducing the likelihood of delays once the application is submitted.

Assess prudential requirements under COREPRU and CRYPTOPRU: The new prudential framework blends traditional principles with crypto specific risk considerations. Firms should assess the impact of capital and liquidity expectations on their business model, ensure they are adequately capitalised, and document their approach to risk measurement and stress testing.

Prepare a high quality, complete application: Applications will need to be clear, coherent and well supported, including a robust Regulatory Business Plan (RBP), detailed financial projections, prudential calculations, outsourcing arrangements, and evidence of SMCR readiness. Strong documentation will materially increase the likelihood of timely authorisation.

As the new UK cryptoasset regime moves rapidly toward implementation, firms that prepare early will be best positioned to enter the new framework smoothly and with confidence. If you would like to know more about the regime or are looking for support in understanding your requirements, please contact us to speak to a member of the team.

Contact us

We're here to help - whether you have a question, need advice, or want to tell us about your requirements.

Sharper perspectives

Financial Services · ICARA and wind-down processes · Insight · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting

A turning point for Form PF reporting

Financial Services · ICARA and wind-down processes · Insight · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting

SMCR reforms: a step towards a more proportionate regime

Financial Services · ICARA and wind-down processes · Insight · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting

AI in asset management: what the FCA expects

Financial Services · ICARA and wind-down processes · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting

Getting your FCA application right in 2026

Financial Services · ICARA and wind-down processes · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting

The most anticipated consultation for UK asset managers in a decade

Financial Services · ICARA and wind-down processes · Insight · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting