Wholesale buy-side firms and wholesale markets: What you need to know

16 Apr 2026 • Financial Services • ICARA and wind-down processes • Insight • Preparation of Disclosures • Prudential Reporting and Advisory • Regulatory Reporting • Thresholds, indicators and OFAR monitoring • Transparency Reporting

In March 2026, the Financial Conduct Authority (FCA) published a series of Regulatory Priorities reports with a clearer and more consistent approach to communicating sector specific expectations.

Replacing the former portfolio letters, these reports set out the FCA’s supervisory and policy priorities for the year ahead, helping firms understand where to focus their efforts and how to align with regulatory direction.

Rather than introducing immediate rule changes, the reports provide a concise statement of the FCA’s current priorities and highlight the areas where boards, senior management, and compliance teams should anticipate regulatory attention over the next 18 months.

A recurring theme is the FCA’s expectation that firms “engage proactively” with ongoing reforms, and participate in regulatory sandboxes and industry initiatives to support the safe and responsible adoption of new technologies.

In this insight, we summarise the key priorities across sectors, with particular emphasis on the reports most relevant to our clients: Wholesale buy-side firms and Wholesale markets.

The FCA’s priorities for Wholesale Buy-Side firms report: A bitesize summary

Smarter, more predictable supervision

The FCA aims to be a data‑driven, proportionate regulator with clearer sector‑level expectations and a focus on innovation, market integrity, and the UK’s global competitiveness.

Modernising regulation for growth

Reform of the Alternative Investment Fund Manager (AIFM) regime and Investment Firm Prudential Regime (IFPR) is underway to make them more effective and proportionate, alongside a major overhaul of asset‑management data to improve accuracy, comparability and risk visibility.

Heightened scrutiny of private markets

Given their systemic importance, the FCA is intensifying oversight of governance, valuations of illiquid assets, and conflicts of interest across private‑market strategies and fee/co‑investment structures.

Strengthening market integrity and resilience

The regulator is targeting risks from leverage, illiquidity, concentrated exposures, and AI‑driven models, while demanding strong operational resilience, cyber controls, and robust market‑abuse detection.

Board accountability for technology and culture

Boards and senior managers must take clear ownership of emerging tech governance (AI and tokenisation), with the Senior Managers and Certification Regime (SMCR) and remuneration rules under review to streamline burden while maintaining accountability. Firms must show strong controls around critical third parties, cyber governance, incident response, stress testing, surveillance, and reporting.

The FCA’s priorities for Wholesale Markets report: A bitesize summary

Strengthening firm and market resilience

The FCA is intensifying its focus on operational resilience after over a quarter of 170 incidents in 2025 were linked to third‑party failures. Priority areas include stronger trading controls, liquidity management, cyber resilience, and oversight of algorithmic trading. New rules on market outage resilience are expected following 2026 disruptions. Firms must materially upgrade resilience, governance, and controls, especially around third‑party risk, market‑infrastructure robustness, and algo‑trading oversight.

Advancing an efficient, competitive, and innovative market structure

Post‑Brexit reforms continue across prospectuses, consolidated tapes, research rules, and client categorisation, with more changes coming in securitisation and commodity derivatives. The FCA is also reviewing wholesale conduct rules, IFPR implementation, and engaging on tokenised securities and the upcoming cryptoasset regime. Firms should actively prepare for regulatory change, respond to consultations, and strengthen governance to meet evolving frameworks.

Enabling safe, responsible use of new technology

The FCA supports responsible adoption of AI, digital assets and quantum technologies, emphasising risk understanding, governance, testing, and safe‑innovation practices. It encourages sandbox participation and will continue monitoring tech use without issuing new AI guidance for now. Firms must enhance governance, risk management, and testing to ensure responsible deployment of emerging technologies.

Tackling financial crime and market abuse

Financial crime remains a core priority: The FCA received 3,806 Suspicious Transaction and Order Reports (STORs) in 2025, with 82% of those linked to insider dealing. Despite some improvements, firms still show material gaps in surveillance, data quality, governance, and reporting. AI may support stronger detection capabilities.

Ensuring strong conflict management and conduct oversight

The FCA is sharpening its scrutiny of conflicts of interest, especially where firms assume new responsibilities or use new technologies. Upcoming work includes reviews of benchmark administrators, non‑financial misconduct controls, Payment for Order Flow (PFOF), pre‑hedging practices, and proportionate Consumer Duty application in wholesale markets. Firms must strengthen conflict‑management and conduct controls to ensure transparent, well‑governed practices.

Timings

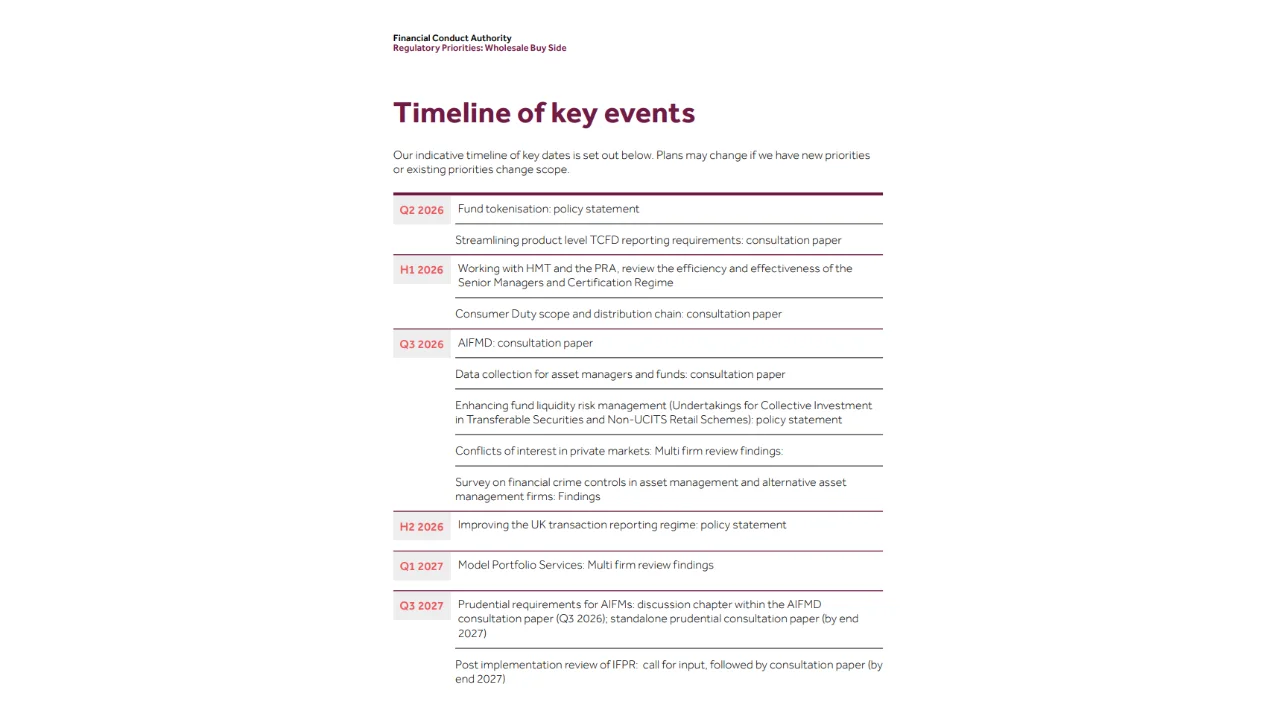

The report highlights several cross-cutting regulatory workstreams covering AIFM prudential reform, a postimplementation review of the IFPR, the ongoing SMCR review, the future regime for Environmental Social Governance (ESG) ratings providers, further cryptoasset policy development, and findings from the FCA’s financial crime survey. It also clarifies that proprietary ESG ratings offered solely as part of an existing regulated activity are not expected to fall within scope of the new ESG ratings regime. The accompanying timeline begins in Q2 2026 not solely in the second half of the year and outlines a steady sequence of consultations, policy statements and supervisory outputs extending through 2026 and 2027.

Wholesale buy-side firms timeline of key events (source FCA)

Wholesale markets timeline of key events (source FCA)

What does this mean for you?

Taken together, the FCA’s priority reports reinforce a clear regulatory trajectory: Firms must align innovation with strong governance, understand the full extent of their Consumer Duty obligations, and ensure that valuation practices and conflicts frameworks particularly in private markets are demonstrably robust. At the same time, operational resilience, cyber readiness and market abuse controls must keep pace with evolving risks.

With an intensive programme of consultations and policy developments scheduled through 2026 and 2027, close horizon scanning by legal and compliance teams will be essential. Overall, the report offers a timely steer on where supervisory scrutiny is heading and the standards the FCA expects firms to prioritise now. If you are concerned about any of the focus areas outlines within the FCA’s priority reports, contact us to speak to a member of our team.

Contact us

We're here to help - whether you have a question, need advice, or want to tell us about your requirements.

Sharper perspectives

Financial Services · ICARA and wind-down processes · Insight · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting

A turning point for Form PF reporting

Financial Services · ICARA and wind-down processes · Insight · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting

AI in asset management: what the FCA expects

Financial Services · ICARA and wind-down processes · Insight · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting

SMCR reforms: a step towards a more proportionate regime

Financial Services · ICARA and wind-down processes · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting

Getting your FCA application right in 2026

Financial Services · ICARA and wind-down processes · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting

The most anticipated consultation for UK asset managers in a decade

Financial Services · ICARA and wind-down processes · Insight · Preparation of Disclosures · Prudential Reporting and Advisory · Regulatory Reporting · Thresholds, indicators and OFAR monitoring · Transparency Reporting