Revenue recognition under the revised FRS 102: What membership organisations need to know

22 Apr 2026 • Charities and Not-For-Profits • Charity and Not-For-Profit Audit

From accounting periods beginning on or after 1 January 2026, organisations applying FRS 102 will be required to adopt a revised approach to revenue recognition.

The revised revenue recognition requirements in FRS 102 are particularly significant for membership organisations, where income streams often involve multiple benefits delivered over time. Organisations will need to apply greater judgement to identify the goods or services being provided and determine when income should be recognised.

This article summarises the key changes, explains the new five‑step revenue recognition model, and explores the practical implications for membership organisations. It also considers how organisations can prepare for implementation and the transition options available.

What is changing?

The revised version of FRS 102 introduces a new, structured model for recognising income from contracts with customers. The changes apply to exchange transactions, where goods or services are provided in return for consideration. They do not apply to non-exchange income such as pure donations or investment income.

Under the previous version of FRS 102, revenue was generally recognised when the organisation was entitled to the income, receipt was probable and the amount could be measured reliably. In practice, many membership organisations recognised subscription income and joining fees on a straight-line basis or, in the case of joining fees, in full, on receipt.

The revised standard replaces this approach with a model that focuses on:

Identifying the promises made to customers

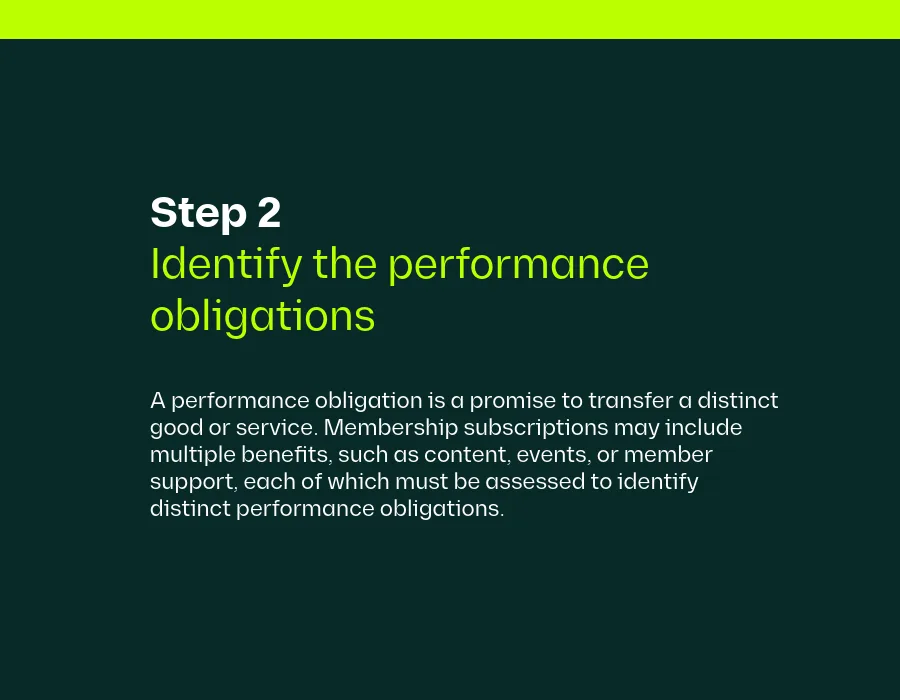

Determining whether those promises are distinct performance obligations

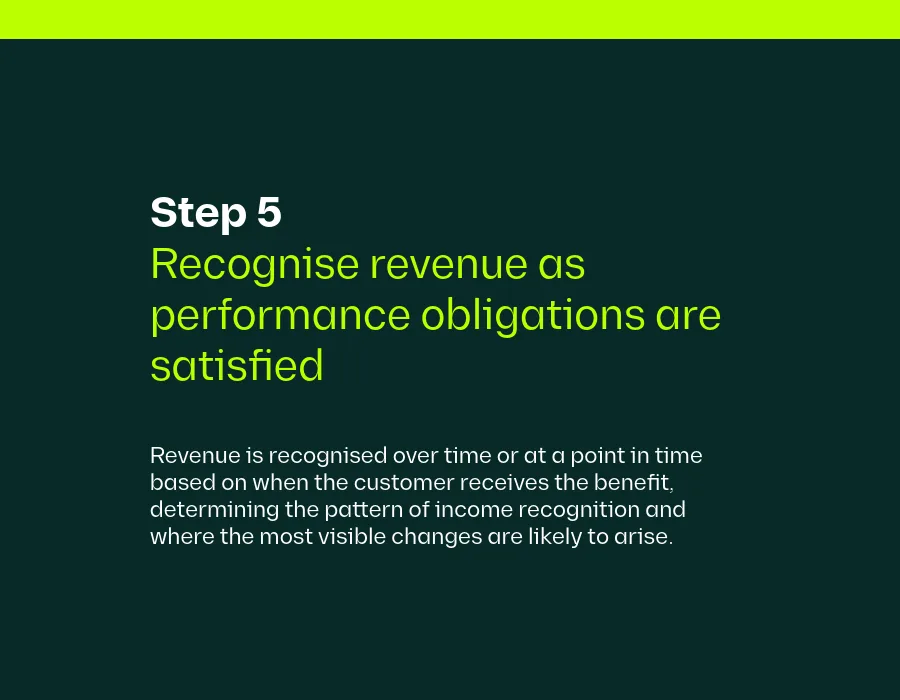

Recognising income as and when those obligations are satisfied.

For some organisations, this change will significantly affect the timing of income recognition, reported surpluses, and opening reserves on transition.

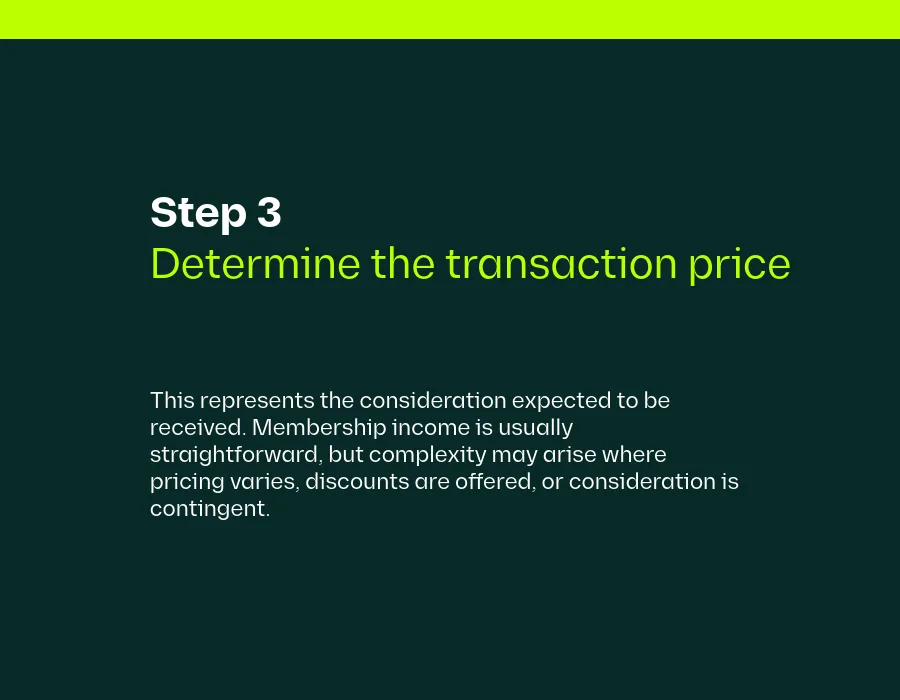

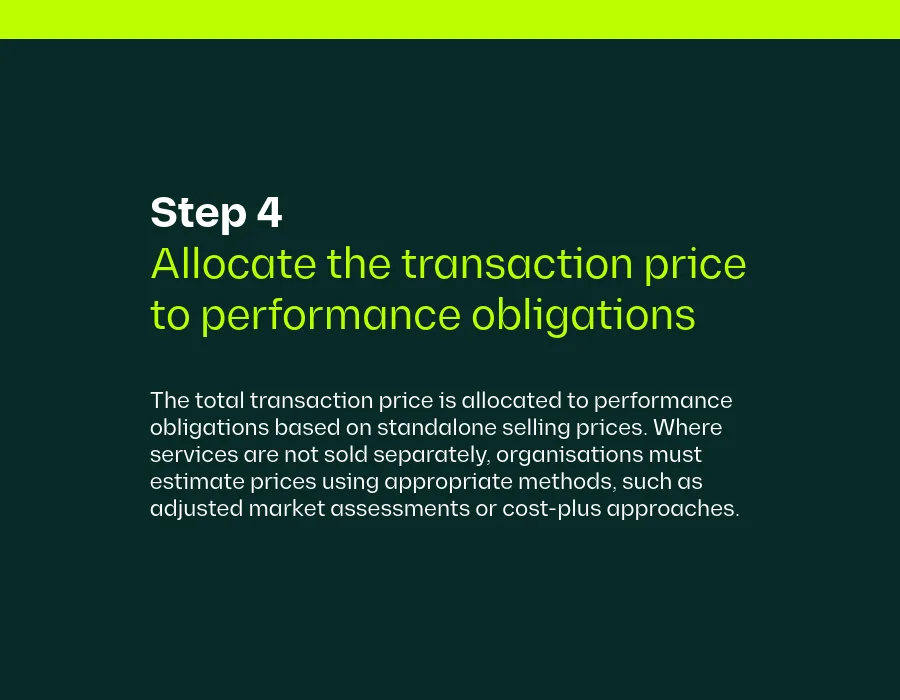

The five-step revenue recognition model

The revised FRS 102 requires organisations to apply a five-step model to all material contracts with customers.

Key challenges for membership organisations

Preparing for implementation

Organisations should not underestimate the work involved in implementing the revised revenue recognition model. Key preparatory steps include:

Identifying all material contracts and income streams

Analysing each contract under the five-step model

Documenting key judgments, assumptions and estimates

Gathering data to support estimates such as average membership tenure

Engaging early with auditors to agree approaches

Accounting policies and disclosures will also need to be updated, with additional transitional disclosures required in the first year of adoption.

Transition and adoption approaches

The revised FRS 102 offers two approaches to adoption:

Full retrospective application, where comparative figures are restated as if the new rules had always applied

Modified retrospective application, where comparatives are not restated and a cumulative adjustment is made to opening reserves at the transition date

The full retrospective approach improves comparability but requires more work and data. The modified retrospective approach is simpler but can result in less meaningful trend information in the year of adoption.

The revised revenue recognition requirements under FRS 102 represent a fundamental shift in how membership organisations account for income. While the changes may not affect the total income recognised over time, they can significantly alter when that income is reported.

With the adoption period already underway, now is the time for organisations to start analysing their income streams, gathering evidence and planning their transition. Early preparation will help avoid surprises at year-end and ensure a smoother adoption of the new standard.

Should you have any questions about how the revised standards will impact you specifically, please don’t hesitate to get in touch via the form below, and one of our specialists will be in touch.

Contact us

We're here to help - whether you have a question, need advice, or want to tell us about your requirements.

Sharper perspectives

Charities and Not-For-Profits · Charity and Not-For-Profit Audit · Insight

Trustees’ Report guidance: What has changed under SORP 2026?

Charities and Not-For-Profits · Charity and Not-For-Profit Audit · Education · Insight

Academy Trust Handbook 2026: What do trusts need to know ahead of 1 October?

Charities and Not-For-Profits · Charity and Not-For-Profit Audit · Education · Insight

Further and Higher Education SORP 2026: Update webinar

Audit and Assurance · Charities and Not-For-Profits · Charity and Not-For-Profit Audit · Insight