Amendments to FRS 102 – what’s new for revenue?

18 Mar 2026 • Audit and Assurance • Audit for Business • Corporate Audit • Insight

Written by

The Financial Reporting Council’s (FRC’s) second periodic review of FRS 102 will become mandatory for reporting periods beginning on or after 1 January 2026.

In addition to key changes to revenue recognition and lease accounting, the amendments also expand the disclosure requirements that businesses reporting under UK GAAP will need to make in their financial statements.

What is changing?

In the second periodic review of FRS 102, Periodic Review 2024, the FRC revised Section 23 Revenue of the standard to Revenue from Contracts with Customers.

These changes will bring UK GAAP in line with International Financial Reporting Standards (IFRS). This alignment extends to the additional disclosure businesses will be required to include in their financial statements. This will mean a longer financial statement preparation process, particularly in the first year if businesses have not prepared appropriately.

Understanding the disaggregation of revenue

Periodic Review 2024 has changed the requirement to disclose revenue in prescribed categories to instead disaggregate revenue in specific categories that depict how economic factors affect revenue and cash flows. This aligns UK GAAP with the disclosures required under IFRS 15, which was a key objective of the periodic review.

This may include:

Major product or service lines

Geographical markets

Type of customer (e.g. sales to public sector and private sector)

Sales made at a point in time vs sales made over time

Revenue earned as an agent or as a principal

The first two categories above suggested by the revised standard will be familiar to those that have prepared financial statements under FRS 102 previously. The additional analysis required can also be presented in tabular disclosures in the revenue note to the financial statements.

Contract assets and liabilities

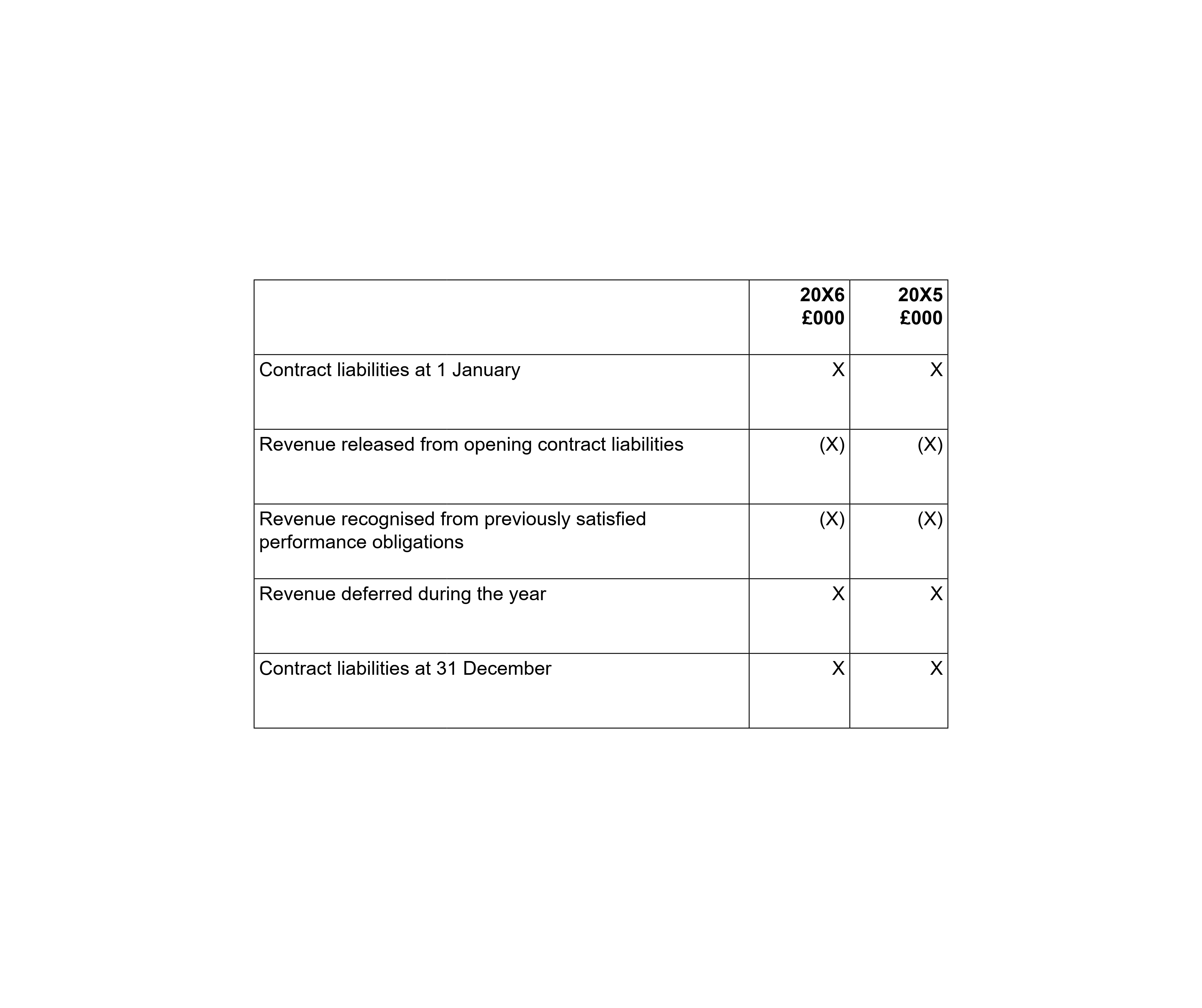

In addition to disaggregation of revenue, businesses with long-term contracts will need to make additional disclosures relating to contract assets and liabilities. These disclosures are a new addition from the periodic review and will enhance transparency to better demonstrate to stakeholders how you generate revenue. The requirements are to report:

Opening balances for any contract assets and/or liabilities.

Revenue recognised during the reporting period that was included within contract liabilities at the start of the reporting period.

Revenue recognised from performance obligations that were satisfied (partially or in full) in prior periods (e.g. from revised estimates in variable consideration).

Closing balances for any contract assets and/or liabilities.

These disclosures may be best presented as a reconciliation of contract balances from the start of the period to the reporting date. For example, as demonstrated below for contract liabilities:

A similar reconciliation will be required for material contract assets.

Performance obligations

The amendments have an additional focus on the identification and financial reporting of performance obligations within a contract. This change addresses the increasingly complex sales arrangements businesses are entering into and the disclosures are written to promote comparability across each entity’s financial statements.

This requires a description of the key information relating to performance obligations in contracts, including:

When they are typically satisfied (e.g. upon shipment, upon delivery, upon completion, over the service period, etc.)

Where performance obligations are satisfied over time, a description of the method used to recognise revenue must be included.

Nature of the goods or service being provided, including any involvement of another party (e.g. if the business is acting as an agent and is not the principal).

Significant payment terms (e.g. when payments are typically due, whether there is variable consideration, whether financing transactions are involved).

Any obligations for returns or refunds.

Any types of warranties offered.

Explanation of any unsatisfied performance obligations, including their significance and when they are expected to be satisfied.

The disclosures on performance obligations will require management to prepare written assessments, with supporting evidence, to provide the appropriate detail in the financial statement notes.

Costs incurred to obtain or fulfil a contract

Sharper perspectives

Audit and Assurance · Audit for Business · Corporate Audit · Risk Advisory and Internal Audits · News · Safeguarding Audits

Buzzacott partners with MindBridge to enhance audit processes with AI-driven analytics

Audit and Assurance · Audit for Business · Business Services · Corporate Audit · Financial Services · Insight · Risk Advisory and Internal Audits

Changes to UK GAAP – should you adopt them early?

Audit and Assurance · Audit for Business · Case study · Corporate Audit · Risk Advisory and Internal Audits

Buzzacott partners with Buck to deliver their AAF report

Audit and Assurance · Audit for Business · Corporate Audit · Financial Reporting and Audit Support · Financial Services · Insight

Accounting for profit allocations in LLPs

Audit and Assurance · Audit for Business · Corporate Audit · Financial Reporting and Audit Support · Financial Services · Hospitality · Insight · Risk Advisory and Internal Audits · Professional Practices · Real Estate and Construction · Technology and Media

Why have a company audit?

Audit and Assurance · Audit for Business · Corporate Audit · Financial Services · Insight